The new budget has been approved by the Board of Trustees and a Special Meeting of the Membership has been called on February 15, 2014 for the purpose of ratifying it.

The following PowerPoint slides are part of Jessica Besso's Budget Q & A session on Saturday, February 2nd, 2014.

See the WRA Calendar for a second, identical, Budget Q & A session is scheduled for February 11th, 2014 at 7:30 pm at the Chalet.

IMPORTANT NOTE:

Jessica's PowerPoint presentation contains a slide showing a Side-by-Side Analysis of Meter Reading and Billing Cost Savings. This slide contains financial information that is available to WRA members only.

To access the slide, you must be a registered website user. For details about how to register, please see How to Access Members-Only Posts

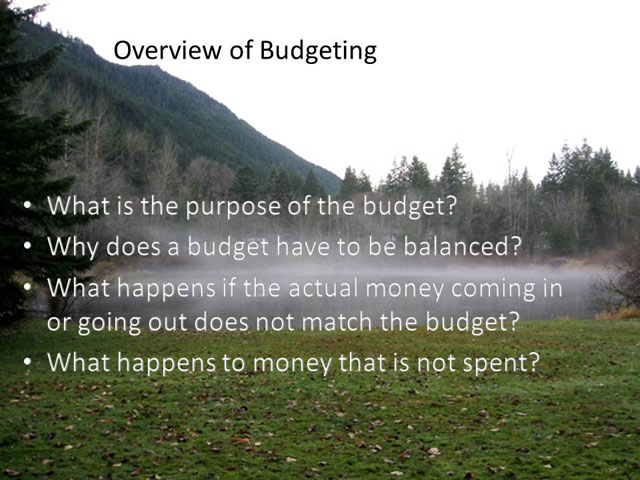

Q: What is the purpose of the budget?

A: The annual budget is a tool for the members and volunteer Board to use as a guideline to direct the Association's income and expenses. It is a way to communicate variances due to reality compared to expectations and hold the volunteer-run committees and membership accountable. It helps everyone plan for the future and prioritize funds as a planning tool and roadmap. The budget provides a control element in financial statements. The budget is used as a guide or “target” to help the homeowner association determine if it has under or over-estimated the amount of the expenditures. If significant deviations from the budget (the expectations of what the expenditures should be) occur, the Board of Trustees should try to determine the causes.

Q: What is a budget not meant to be?

A: A budget is NOT a mandate from the membership. Budgets help minimize the unexpected, but they cannot predict the future. No budget will perfectly align with actual activity, but the intent is to estimate as closely as possible.

Q: Why does a budget have to be balanced?

A: The money coming in and money going out must be equal. The Association cannot plan to spend more money than comes in (a deficit) nor plan to receive more than it spends (a surplus). As a not-for-profit corporation, the bottom line must equal zero.

Q: What happens if the actual money coming in or going out does not match the budget?

A: The Board should determine why there is a large variance and seek corrective measures if necessary. Many factors can cause a budget line item to be greater than or less than the actual amount. Again, a budget is just a working estimate or goal.

Q: What happens to money that is not spent?

A: The Board evaluates the financials on a quarterly basis and can allocate funds for reserves, capital improvements, repairs, or other future needs.

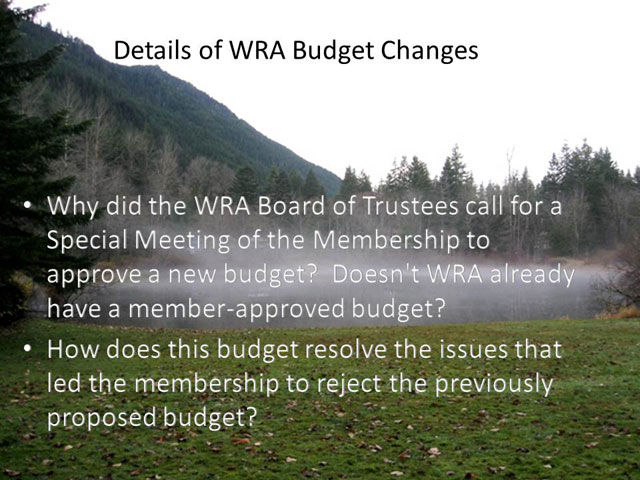

Q: Why did the WRA Board of Trustees call for a Special Meeting of the Membership to approve a new budget? Doesn't WRA already have a member-approved budget?

A: The members rejected the budget proposed at the July 2013 annual meeting.

RCW 64.38.025 requires that the corporation use the last budget approved which was the 2012-13 budget. The membership should have clear communication from the Board on financial matters, and the only way to do that is through a special meeting. Washington State law requires that any budget the Board adopts must be ratified by the membership. The Board wants the membership to be aware of the financial commitments it is making. The new budget reflects a better estimate of income and expenses and includes costs that have already been incurred that were not part of the budgets in prior years such as the reserve study and financial statement audit.

Q: How does this budget resolve the issues that led the membership to reject the previously proposed budget?

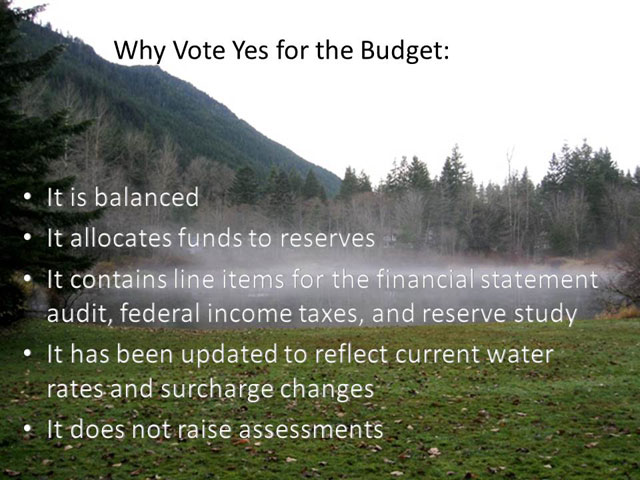

A: The budget is balanced, aligns more accurately with actual expenses, allocates funds to the reserve accounts from surcharge, and does not raise assessments.

Q: Why is WRA performing the billing and meter reading instead of Sallal? Was there something that happened with Sallal?

A: The renewal of our contract comes up every January. In the process of preparing for that renewal, it was decided that preparing the billing and meter reading is more cost-effective for the membership when performed by our own staff. Also the Board had been advised by the outside independent auditors and CPA who prepares the tax returns that the billing records should be in the control of WRA. Other benefits of moving the work in house include adherence to the WRA Water Regulations, better service to the membership with integration of assessment and water billing, and cost savings of $10,000-$15,000/year. Detailed analysis of the cost savings is available in the office or in the members-only area of the website.

Q: Are my water rates going to be impacted by this change with Sallal? How will my water bill be affected by the new budget?

A: The intent is to keep costs reasonable and reduce where possible. The water rate increase last fall is the basis of the revenue projections in the budget. Actual water consumption will determine actual revenue and whether or not expenses are covered. In dry years, more water is used and is a large variable affecting billing, and bottom line surplus or shortage. We currently do not anticipate any rate changes for the remainder of this calendar year at this time.

Q: Is Sallal continuing to do maintenance on the water system?

A: Yes, we are renewing the contract with Sallal Water Association for the Water System Operator, Denny Scott, for 2014.

Q: Will the billing be accurate? What about the meter readings?

A: The Association has employed an administrative assistant to handle all day-to-day office operations for some time, and now water billing will again be among the list of duties. The training for billing is included in the software license fee for the software that we own and used in the past. Meter reading is not a professional skill. The Association has retained the services of a competent meter reader who is supported by our Water System Operator through our contract with Sallal Water Association.

Q: What if the meter reader is ill? Is there a backup plan?

A: The readings do not have to be performed on particular days of the month. The Water Committee and Board of Trustees fully support this effort that saves the membership over $5,000 and will ensure that the meters are read in a timely and appropriate manner.

Q. What are the reserve funds?

A: The reserves were established decades ago for the purpose of repairing or making capital improvements to the water system or replacing it entirely in the event of a catastrophe.

Q. What are the reserve study requirements?

A: Per RCW 64.38.065, an association is encouraged to establish a reserve account with a financial institution to fund major maintenance, repair, and replacement of common elements. The Board of Trustees is responsible for administering the reserve account. The Association is currently funding replacement reserve accounts for the future major repair and replacement of Association assets of the water system. Accumulated funds are held in separate accounts and are generally not available for operating purposes. There is a reserve study being prepared by FCS Group using the calendar year 2013 water operations data.

Q: What happened to the reserves in prior years?

A: The 2012-2013 fiscal year budget approved by the membership does not include the allocation of the Water Surcharge income to the Water Reserve. Therefore, the membership approved the decision of the 2011-2012 Board of Trustees to opt out of the regulation and to use the funds for necessary operational costs. Controls are being put in place to educate the Board and future volunteers on how the reserves need to be funded, currently per the Water Regulations via the surcharge. This proposed budget meets this requirement.